REVIEW AND OUTLOOK

After several consecutive relatively quiet quarters, the first quarter of 2022 saw the return of the bear market in both bonds (worst correction in the last 50 years) and equities (Nasdaq, EuroStoxx 50, CSI 300…).

This negative trend has continued since the beginning of Q2 2022. Equity indices are still falling (S&P500 -8.8%, Nasdaq -13.3% in April) and the rise in bond yields is accelerating (US 10-year from 2.3% to 2.9% in April, Bloomberg Global Aggregate Index -11.3% YTD including -5.5% in April alone!).

Finally, the outlook remains mixed. Inflation persists and will start to impact corporate margins and household consumption, central banks will continue to reduce their accommodative policies, geopolitical tensions may persist, and the pandemic is resisting in China. The end of the economic cycle is accelerating, and fears of a recession are growing rapidly.

Against this backdrop, the Quadra team reiterates the importance of focusing on strategies that preserve capital while generating performance.

As we take stock of the year and despite this uncertain environment our liquid Credit/Event Driven strategies are performing well, and our Private Equity/Real Assets funds continue to deploy their capital through targeted investments.

OUR LIQUID STRATEGIES

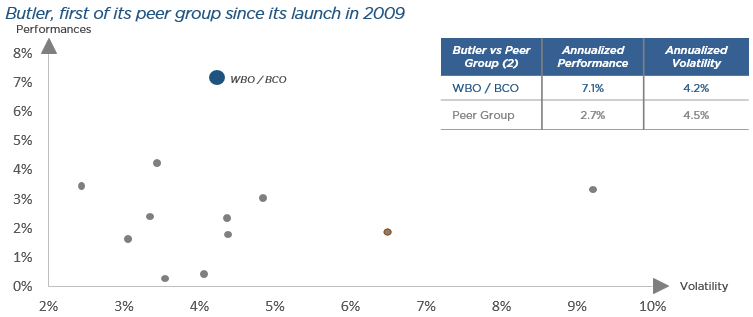

- Butler Credit Opportunities : the UCITS Long-Short Credit High Yield fund outperformed its benchmark every month this quarter and lost only 1.09% vs. Markit IBoxx EUR HY at -4.59%. Outperformance continues in April. This strategy has never had a negative year since its launch in 2009 and has just been soft-closed. It remains very relevant within the bond allocation to reduce duration and cushion interest rate shocks.

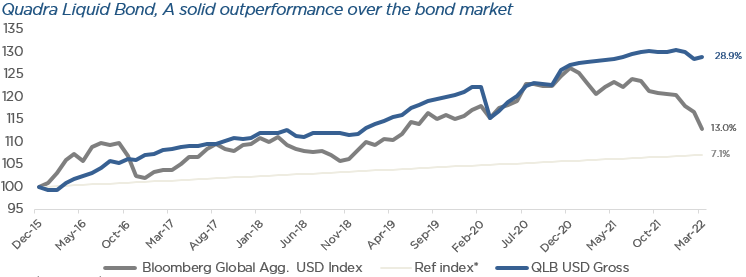

- Quadra Liquid Bond : The idea of this fund is to select successful European managers, unknown in Canada, to deliver a performance of +4 or 5% on average per year through a combination of several low-risk strategies. In a challenging market our Fixed Income Blend solution was down -1.85% over 2022 and managed to outperform the Global Aggregates index by more than 850 bps.

OUR PRIVATE EQUITY / TANGIBLE ASSETS STRATEGIES

- Flexam Invest : The raising of the second fund is going very well. The pace of capital deployment remained strong in Q1 2022 with a new investment in 2 hybrid-powered vessels to transport personnel and equipment to wind farms located in the North Sea. High and secure yield (10%+ in the family office version, 5-6% in the institutional version with an SCR <10%) while financing assets in healthcare and ecological transition. In the very tough fixed income environment of 2022, the 8% annual cash yield makes this strategy a great alternative in fixed income investments.

- Geneo : The fund’s purpose is to “provide invested SMEs and SMIs with the means to achieve their ambitions, in a sustainable and positive impact approach”. The fund’s assets exceed 400 million euros and 14 investments have already been made.

CONCLUSION

Congratulations to our teams and partners strategies for their performance and resilience in such a difficult context! We also thank all our European and Canadian investors for their trust.

We are looking forward to coming back to you soon to announce new developments in our offering in Europe and Canada with new partners! We also remain at your disposal in case of questions or to discuss our products in more detail.

KEY GRAPHS

Source: Butler Investment Managers and Bloomberg. As of 31/03/2022. The performance of WBO/BCO is represented by the USD A2 share class of the WBO fund since inception on the 01/10/2009 till 31/05/2017, then by the EUR Institutional Founder (ISIN: IE00BMVX1R57) of the BCO fund from 01/06/2017 till as of date. BCO investments present a risk of loss of capital and their liquidity may be limited. Income is not guaranteed and depends on the evolution of the financial markets and/or exchange rates. These performance figures refer to the past and past performance is not a reliable guide to the future performance. Since WBO inception 01/10/2009

* Ref index: €STR + 150 bps

Source Apex / Quadra Capital Partners / Bloomberg. As at 31/03/2022. Blend simulated performance calculated with the allocation as of 31/12/2021. Live performance since April 2021. Past performance is not a reliable indicator of future results and investors may not get back amount originally invested

New financing agreement with Danish subsidiary NORTHERN OFFSHORE SERVICES for the acquisition and conversion of 2 crew transport vessels (CTV). The two vessels, built in 2016 by the Piriou shipyards, will have their diesel engines replaced by a hybrid motorization allowing the transport of personnel and equipment to offshore wind farms.

DISCLAIMER

Quadra Capital Partners LLP is registered in England and Wales and is authorised and regulated by the Financial Conduct Authority. In accordance with the SYSC 10A rule of the FCA handbook calls will be recorded. Copyright material and/or confidential and/or privileged information may be contained in this e-mail and any attached documents. The material and information is intended for the use of the intended addressee only. If you are not the intended addressee, or the person responsible for delivering it to the intended addressee, you may not copy, disclose, distribute, disseminate or deliver it to anyone else or use it in any unauthorised manner or take or omit to take any action in reliance on it. To do so is prohibited and may be unlawful. The views expressed in this e-mail may not be those of the Company from which it has come but the personal views of the originator. If you receive this e-mail in error, please advise the sender immediately by using the reply facility in your e-mail software. Please also delete this e-mail and all documents attached immediately.

Quadra Capital Partners France has a non-independent consulting activity. Thus, it may receive retrocession from the funds managers that Quadra selected for its customers. These retrocessions do not affect its analysis of these funds’ features and its ability to report on them, the strengths as the risks, in a full transparency to its clients and in their best interest.

Quadra Capital Partners LLP is registered in England and Wales and is authorised and regulated by the Financial Conduct Authority. In accordance with the SYSC 10A rule of the FCA handbook calls will be recorded. Copyright material and/or confidential and/or privileged information may be contained in this e-mail and any attached documents. The material and information is intended for the use of the intended addressee only. If you are not the intended addressee, or the person responsible for delivering it to the intended addressee, you may not copy, disclose, distribute, disseminate or deliver it to anyone else or use it in any unauthorised manner or take or omit to take any action in reliance on it. To do so is prohibited and may be unlawful. The views expressed in this e-mail may not be those of the Company from which it has come but the personal views of the originator. If you receive this e-mail in error, please advise the sender immediately by using the reply facility in your e-mail software. Please also delete this e-mail and all documents attached immediately.

Quadra Capital Partners France has a non-independent consulting activity. Thus, it may receive retrocession from the funds managers that Quadra selected for its customers. These retrocessions do not affect its analysis of these funds’ features and its ability to report on them, the strengths as the risks, in a full transparency to its clients and in their best interest.

Additional Information for Canadian Investors

An investment in the shares of the fund mentioned in this document is only available to an investor who is: (a) an “accredited investor” within the meaning of National Instrument 45-106 – Prospectus Exemptions who is subscribing to the shares of the fund mentioned in this document and any subsequent shares as principal for its own account and not for the benefit of any other person; and (b) a “permitted client” within the meaning of National Instrument 31-103 – Registration Requirements, Exemptions and Ongoing Registrant Obligations.

Securities legislation in certain provinces or territories of Canada may provide an investor with remedies for rescission or damages if this document contains a misrepresentation, provided that the remedies for rescission or damages are exercised by the investor within the time limit prescribed by the securities legislation of the investor’s province or territory. The investor should refer to any applicable provisions of the securities legislation of the investor’s province or territory for particulars of these rights or consult with a legal advisor.